Buying a property from a Non-Resident Indian (NRI) seller is not just about sealing a deal; it involves navigating a unique set of tax regulations, legal requirements, and compliance protocols. Here’s a comprehensive guide to help you handle this process seamlessly and avoid common pitfalls.

- TDS and Tax Compliance

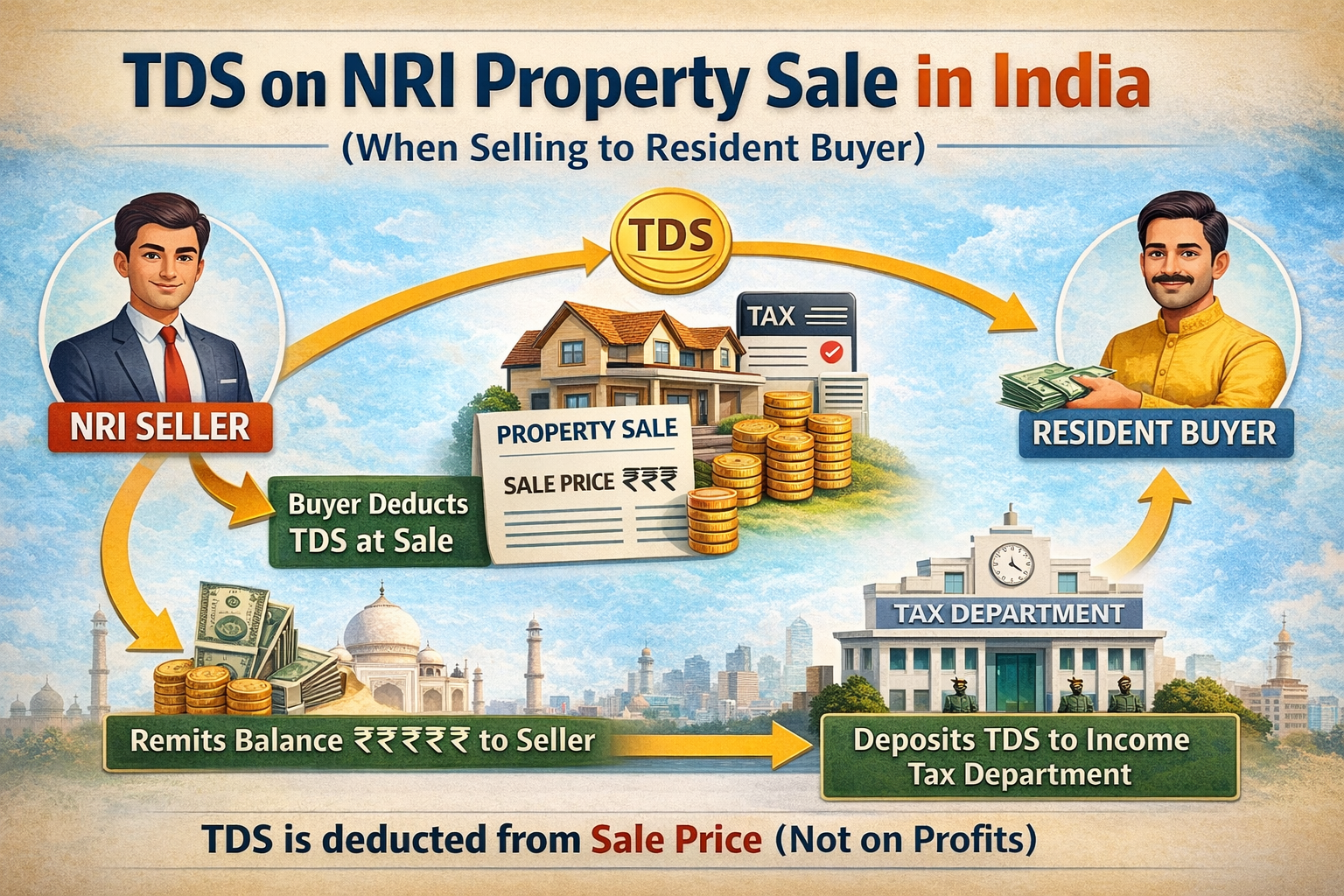

One of the most significant distinctions when buying property from an NRI seller is the rate and handling of Tax Deducted at Source (TDS).

- For resident sellers, TDS is 1% of the property value if it exceeds ₹50 lakh.

- For NRI sellers, the TDS rate starts at 12.5% and can increase depending on the sale value, including surcharges and cess. Importantly, this TDS is calculated on the entire sale consideration, not just the capital gain.

Buyers must file Form 27Q to report TDS for NRI sellers, as opposed to Form 26QB for resident sellers.

- TAN Requirement for Buyers

As a buyer, you need to obtain a Tax Deduction and Collection Account Number (TAN) to report and deposit TDS for an NRI seller. This number is different from your PAN and is essential for compliance.

Tip: Apply for TAN early, as the processing can take 1-2 weeks. Non-compliance in deducting or depositing TDS could lead to penalties.

- Payment Protocols

Payments must be routed to the NRI seller’s NRO, NRE, or FCNR accounts as per FEMA regulations. Avoid transferring funds to their regular savings accounts, as NRIs are not permitted to maintain such accounts. Typically, payments are made to their NRO account.

- Handling Power of Attorney (PoA)

If the NRI seller cannot be physically present, they may authorize someone in India through a Power of Attorney (PoA). Ensure that the PoA is:

- Notarized and attested by the Indian consulate in the seller’s country.

- Valid and specific to the transaction.

Even with a PoA, TDS must be deducted at NRI-specific rates. Verify all documents carefully before proceeding.

- Co-Ownership Considerations

When a property has co-owners, each owner’s share should be explicitly mentioned in the sale deed. TDS must be deducted based on their respective ownership percentages and residential status. For example:

- If one co-owner is an NRI and the other a resident, TDS must be calculated separately at rates applicable to each.

- Lower TDS Deduction Requests

An NRI seller may apply for a lower TDS deduction certificate from the income tax department. If they do:

- Verify the certificate’s authenticity before adjusting the TDS rate.

- Provide necessary documents, such as your TAN, the sale agreement, and payment receipts.

Failure to follow this protocol can result in future disputes with tax authorities.

- Document Verification and Legal Due Diligence

Meticulous documentation is crucial in property transactions with an NRI seller. Ensure you:

- Verify the title deed to confirm clear ownership.

- Check for any existing loans or encumbrances on the property.

- Validate the seller’s PAN card.

- Confirm there are no pending taxes or legal disputes tied to the property.

- Penalties for Non-Compliance

Failure to comply with TDS requirements can lead to severe penalties:

- 1% interest per month for non-deduction.

- A penalty equal to the TDS amount if not deposited.

- Additional late fees for delayed TDS return filings.

To avoid such penalties, ensure timely deduction, deposit, and reporting of TDS.

- Filing Income Tax Returns

Buyers are advised to file income tax returns even if their income is below the exemption limit. Tax authorities may issue notices if the source of funds for the purchase isn’t clear. Always ensure that your income source aligns with the sale consideration.

- Maintaining Records for the Future

Keep the following documents securely for future reference:

- Sale deed and purchase agreements.

- Loan allotment and disbursement details.

- Payment receipts and bank statements.

- Copies of filed TDS returns and associated certificates.

These records can help resolve any future queries or disputes.

Final Thoughts

Purchasing property from an NRI seller involves additional layers of compliance, but with proper preparation and attention to detail, it can be a smooth process. If you’re unsure about any aspect, consult a professional to guide you through the legal, financial, and procedural nuances.

By following these steps, you can make your dream property purchase a reality without unnecessary complications.

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}