To simplify tax collection, the Income Tax Department mandates TDS deductions for certain property transactions. According to the Finance Act, 2013, individuals or HUFs purchasing property worth ₹50 lakh or more must deduct TDS while making payments to the seller. This tax must be deposited using Form 26QB within the specified timeframe.

Here’s a comprehensive guide to understanding and filing Form 26QB.

What Is Form 26QB?

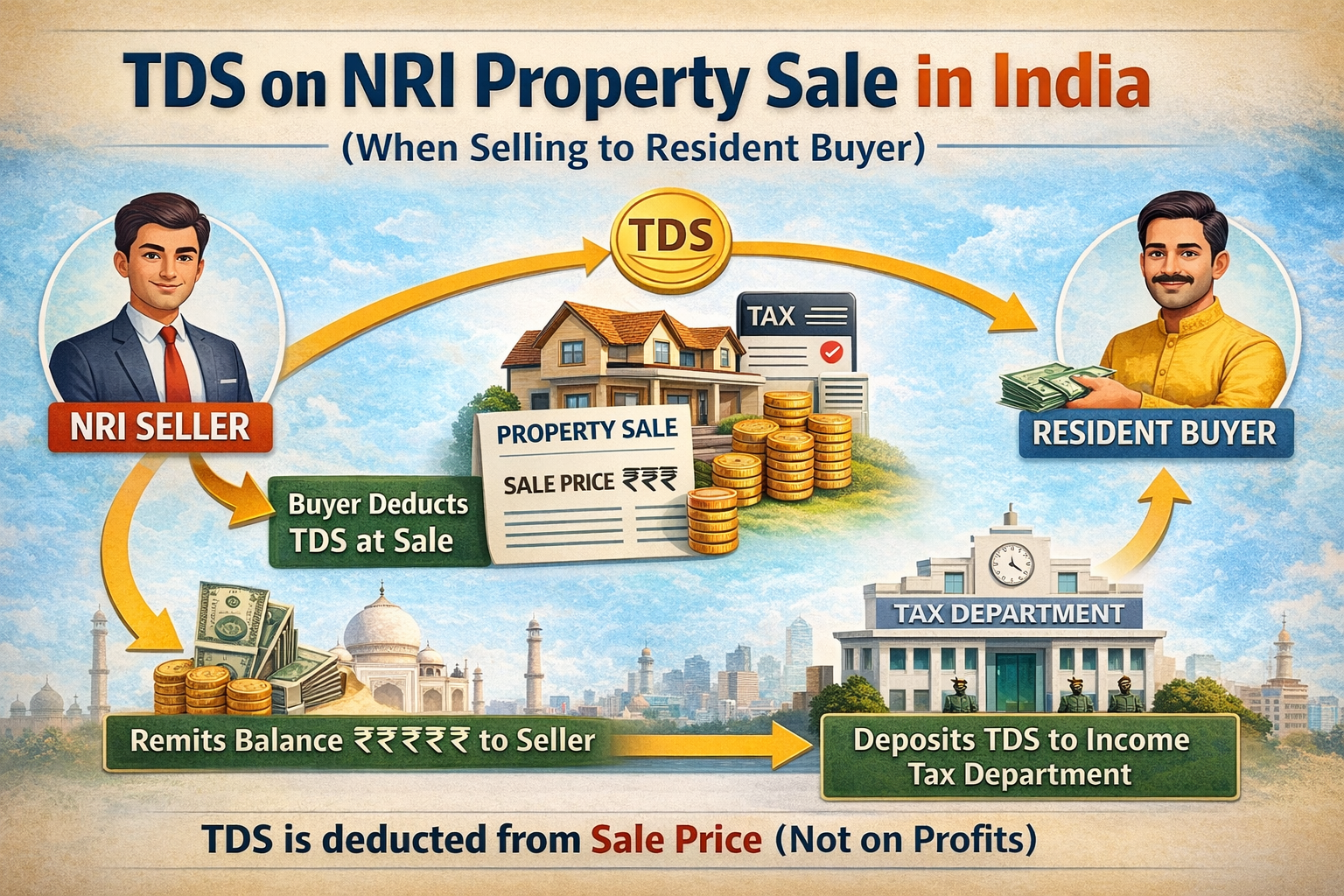

Under Section 194-IA of the Income Tax Act, buyers must deduct TDS at 1% of the property's transaction value or its stamp duty value, whichever is higher, if the property’s value exceeds ₹50 lakh.

For instance, if a property is purchased for ₹80 lakh, the TDS is calculated on ₹80 lakh, not ₹30 lakh (₹80 lakh minus ₹50 lakh).

Form 26QB serves as a combined challan and statement for paying this TDS. Buyers are required to submit this form online, providing details about the transaction, property, buyer, seller, and TDS deposit.

Types of Properties Covered

TDS applies to various immovable properties, including:

- Residential houses

- Commercial establishments

- Plots of land without any construction

- All other immovable properties except agricultural land

This rule is applicable only when the total transaction value of the property is ₹50 lakh or above.

Special Considerations for Non-Agricultural Land

Land is considered non-agricultural if it meets these criteria:

- Located in an urban area under a municipality or cantonment board with a population exceeding 10,000.

- Situated within specific distances from urban boundaries:

- 2 km for populations of 10,000–1,00,000

- 6 km for populations of 1,00,000–10,00,000

- 8 km for populations above 10,00,000

How TDS is Calculated?

TDS is deducted based on the higher value between the property’s sale price and its stamp duty valuation. If the property’s value exceeds ₹50 lakh, the TDS is calculated on the full amount, not just the portion above ₹50 lakh.

Example:

Suppose Ms. R purchases a property from Mr. L for ₹85 lakh, but the stamp duty value of the property is ₹90 lakh. In this case, the TDS will be calculated on ₹90 lakh, resulting in a deduction of ₹90,000. After this, Mr. L will receive ₹84.1 lakh.

When Should Form 26QB Be Filed?

Buyers must file and submit Form 26QB within 30 days from the end of the month in which the TDS was deducted. For instance, if the transaction occurs on December 15, 2023, the TDS must be deposited by January 30, 2024.

Essential Rules Under Section 194-IA

- Deduction of TDS

- Buyers must deduct TDS at the time of payment.

- No deduction is required for property transactions below ₹50 lakh.

- No Requirement for TAN

- A Tax Deduction Account Number (TAN) is not mandatory for buyers.

- However, PAN details of both buyer and seller must be provided.

- Transactions with Multiple Buyers or Sellers

- Each buyer-seller pair must file a separate Form 26QB in cases with multiple parties.

- Payment in Instalments

- TDS should be deducted proportionally with every instalment.

- Issuance of TDS Certificate

- After depositing the TDS, buyers must issue Form 16B to the seller within 15 days.

- Agricultural Land Exemption

- TDS is not applicable on agricultural land unless it falls outside the definition of agricultural property.

Filing Form 26QB: Step-by-Step Process

- Visit the Income Tax Website:

Log in to the official income tax portal. - Access the E-Pay Section:

Navigate to the "E-file" tab, choose "e-pay Tax," and select "26QB - TDS on sale of property." - Complete Property Details:

Fill in the buyer's and seller's basic details, property information, and payment particulars. - Select Payment Method:

Choose between "Pay Now" or "Pay Later" for the TDS amount. - Submit and Download Acknowledgment:

After payment, download the Form 26QB acknowledgment receipt. - Generate TDS Certificate:

Log in to the TRACES portal to download Form 16B, the TDS certificate, for issuing to the seller.

Where can the TDS Deducted on the Property be Seen by the Seller?

TDS deducted will be reflected in Form 26AS Part F

Penalty for Non-Compliance

| Reason | Penalty |

| Delay in filing TDS | ₹200 per day (Section 234E) |

| Non-remittance of deducted TDS | 1.5% interest per month on unpaid TDS |

| Failure to deduct TDS | 1% interest on the un-deducted amount |

| Not submitting the required statement | Penalty of ₹10,000 to ₹1,00,000 under 271H |

Conclusion:

Form 26QB is critical for ensuring TDS compliance during property transactions. Buyers should meticulously file the form within the specified timeline to avoid penalties. Proper understanding of TDS deduction rules simplifies the process and ensures smooth completion of transactions.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}