Selling property in India as a Non-Resident Indian (NRI) involves several tax and legal obligations, with Tax Deducted at Source (TDS) being a key component. This article provides an in-depth overview of how TDS works on property sales by NRIs, how it differs from capital gains tax, and what steps can be taken to ensure smooth compliance.

Understanding the Basics: TDS vs Capital Gains Tax

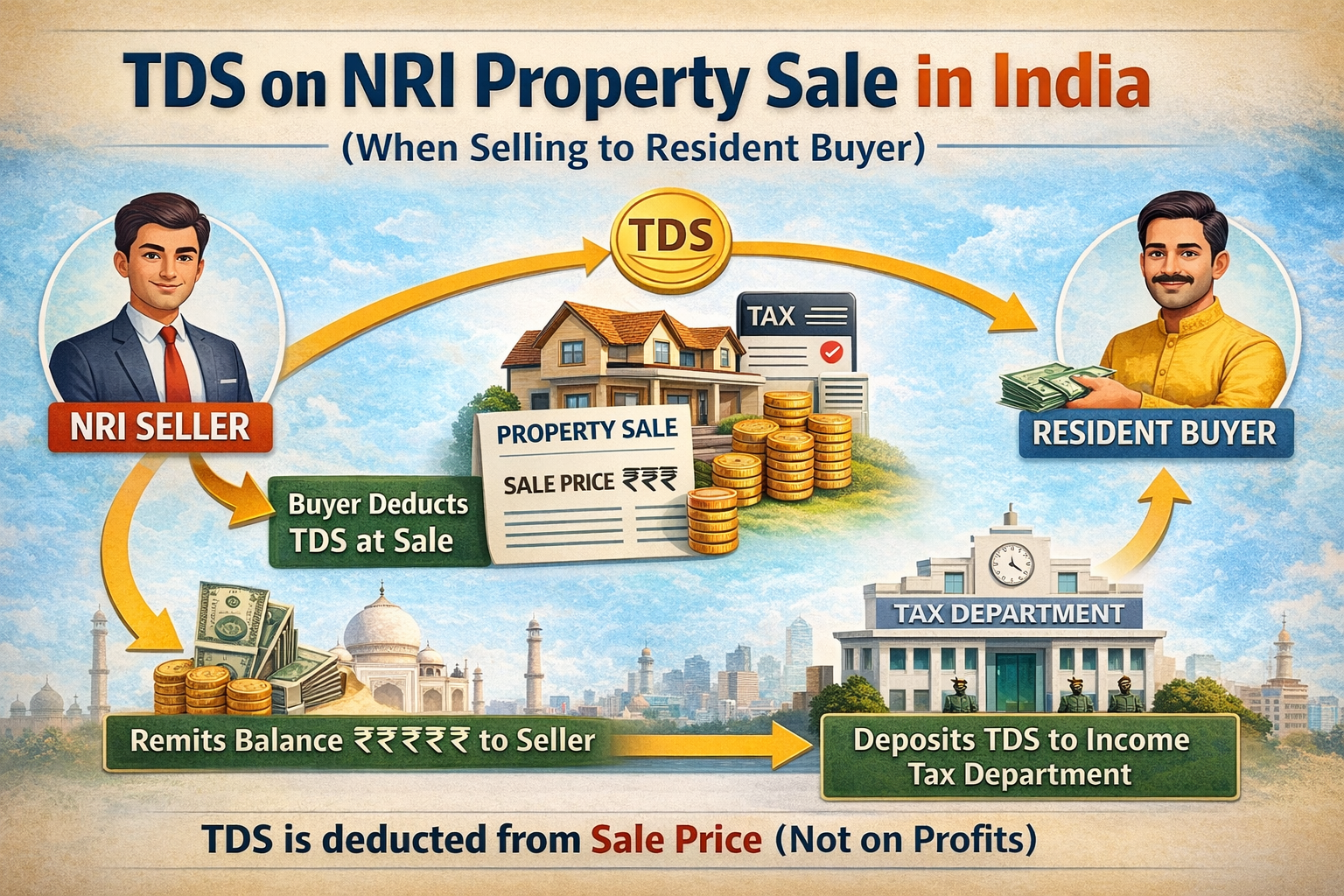

TDS, or Tax Deducted at Source, is a tax that the buyer of the property is legally required to deduct at the time of payment to the NRI seller. Importantly, TDS is calculated on the entire sale consideration, not just the profit.

In contrast, capital gains tax is computed based on the actual profit—i.e., the difference between the sale value and the indexed cost of acquisition (along with allowable deductions). Capital gains are assessed at the time of filing the Income Tax Return (ITR) after the financial year ends.

In most cases, the TDS deducted at the time of sale exceeds the final capital gains tax liability. Therefore, filing the ITR is essential to claim a refund of any excess TDS paid.

Revised TDS Rates (Effective from 23rd July 2024)

Recent changes in tax laws have introduced new TDS rates applicable to NRIs selling long-term capital assets (held for more than two years):

| Sale Value | Previous TDS Rate | New TDS Rate |

| Up to ₹50 Lakhs | 20.8% | 13% |

| ₹50 Lakhs – ₹1 Crore | 22.88% | 14.3% |

| Above ₹1 Crore | 23.92% | 14.95% |

For short-term capital assets (held for less than 2 years), the TDS is applicable at 30% plus surcharge and cess.

Even when the property value is below ₹50 lakhs, TDS is still applicable if the seller is an NRI. In such cases, the buyer must deduct tax using Form 27Q (not Form 26QB, which is meant for resident sellers).

Lower/Nil TDS Certificate: Application Process

NRIs can apply to the Income Tax Department for a Lower or Nil TDS Certificate under Form 13 to reduce the TDS burden at the time of sale.

Required Documents:

- PAN card

- Initial Sale Agreement or Memorandum of Understanding (MoU)

- Proof of purchase cost (builder receipts, payment proof, etc.)

- Capital gains calculation

- Previous years' ITRs

- Buyer's TAN (Tax Deduction Account Number)

It is advisable to initiate this process well in advance, as it typically takes around four weeks for the certificate to be issued. The buyer can deduct TDS at the reduced rate only after receiving this certificate.

Buyer’s Obligation to Obtain TAN

The buyer must have a valid TAN to deposit TDS on behalf of the NRI seller. Many buyers are unaware of this requirement. In such situations, the seller should either guide the buyer or seek assistance from a professional to ensure compliance.

Executing Power of Attorney (PoA)

If the NRI seller is unable to be physically present in India for property registration, a Power of Attorney (PoA) can be executed in favour of a family member, friend, or legal representative in India.

It is essential to consult a legal expert to draft and notarize the PoA appropriately. However, even when a PoA holder conducts the transaction, the primary responsibility for tax compliance remains with the NRI seller.

Receiving Sale Proceeds and Repatriation

The proceeds from the property sale must be deposited into the seller’s Non-Resident Ordinary (NRO) account.

For repatriating funds abroad:

- NRIs can remit up to USD 1 million per financial year

- Banks generally require Form 15CA and Form 15CB, the latter being certified by a Chartered Accountant

- Sellers must maintain records of documents like the sale deed, purchase cost proofs, and tax payment confirmations

Proper documentation ensures a smooth remittance process and helps avoid delays or regulatory hurdles.

Important Documents and Legal Due Diligence

Before initiating the property sale, it is important to ensure that all relevant documents are in order.

Key Documents to Keep:

- Original Sale Deed and Purchase Agreement

- Builder receipts and payment proofs

- Capital gains computation sheet

- TDS Certificate (Form 16A)

- Lower/Nil TDS Certificate (if obtained)

- Form 15CA and 15CB

- NRO/NRE account statements

- PAN card and KYC documents

Form 16A, the TDS certificate from the buyer, is issued after the end of the quarter in which TDS is deducted. This document is crucial, as it enables the seller to claim TDS credit in Form 26AS, and ultimately in their ITR.

Income Tax Return Filing

Regardless of whether the NRI has any other income in India, it is mandatory to file an ITR in the year of property sale.

The return should include:

- Declaration of capital gains (long-term or short-term)

- Claim of exemptions, if applicable (e.g., reinvestment in another property or specified bonds under sections like 54, 54EC)

- Request for refund of excess TDS, if any

Common Mistakes to Avoid

NRIs often face challenges during property transactions due to avoidable errors. Here are some common pitfalls:

- Not applying for a Lower/Nil TDS Certificatein time

- Allowing the buyer to deposit proceeds into a regular savings accountinstead of an NRO account

- Failing to file the ITR after the sale

- Not collecting TDS Certificate (Form 16A)from the buyer

- Not maintaining a proper record of documentsfor future reference or tax audits

Conclusion

The process of selling property in India as an NRI demands careful planning, proper documentation, and timely tax compliance. Buyers and sellers must work closely to ensure that all statutory obligations, particularly around TDS, are met without delay.

Engaging a qualified tax or legal professional early in the process can help avoid complications and ensure a smooth and compliant transaction.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}