As a property owner in India, understanding the tax implications of rental income is essential. The Income Tax Act of 1961 outlines specific parameters for calculating the total taxable income from rental properties, with the gross annual value (GAV) being the starting point. This article provides an in-depth overview of the various income types, calculation processes, and updates from the Union Budget 2024-25 regarding rental income taxation.

Types of Income under the Income Tax Act

The Income Tax Act divides the income received by an individual into five heads, which helps streamline tax computation. These heads are:

- Income from Salary

- Income from House Property

- Income from Profits and Gains of Business or Profession

- Income from Capital Gains

- Income from Other Sources

Typically, rental income from residential properties is categorized under 'Income from House Property.' The tax on rental income is calculated after allowing deductions for municipal taxes, standard deductions, and interest paid on home loans. Let’s delve deeper into the specifics of 'Income from House Property.'

What is Taxable under 'Income from House Property'?

Not all rental incomes fall under the head 'Income from House Property.' Below is a breakdown of what is taxable and what is not:

Taxable under Income from House Property:

- Rental Income from House Property: Rental income received from a house, apartment, or land is taxable under the head 'Income from House Property.'

- Rental Income from Partially Self-Occupied Property: When a portion of the property is occupied by the owner while the remaining portion is rented out, income from the let-out portion is taxed under this head.

Not Taxable under Income from House Property:

- Rental Income from Sub-Leasing: Rental income earned by a tenant from sub-letting the property is not taxed under this section.

- Rental Income from Composite Rent: When a property is rented out with additional assets like washing machines or televisions, the rent for the property is taxed under 'Income from House Property,' while the rent for the assets is taxed under 'Income from Other Sources' or 'Profits and Gains of Business or Profession.'

- Rental Income from Commercial Property with Integrated Assets: If the assets and property are inseparable (such as in the case of a fully equipped theatre), the rent is taxed under 'Income from Other Sources.'

Under Which Section is Income from House Property Taxed?

According to the Income Tax Act, rental income is taxed under Section 22. For the income to be taxable under this section, the following conditions must be met:

- There must be a physical property that includes a building or land attached to it.

- The property should be owned by the taxpayer.

- The property should not be used for business or professional purposes.

Is GST Applicable on Rental Income?

- Residential Properties: Rental income from residential properties is exempt from Goods and Services Tax (GST).

- Commercial Properties: However, rental income from commercial properties is subject to GST at a rate of 18%.

How is Income Tax on Rental Income Calculated?

The tax calculation on rental income involves a series of steps:

- Gross Annual Value (GAV): Calculate the total annual rent received from the tenant.

- Net Annual Value (NAV): Subtract the municipal taxes or property taxes paid from the GAV. This gives the NAV.

- Standard Deduction: Deduct 30% of the NAV, as per Section 24A of the Income Tax Act, as a standard deduction for repairs and maintenance.

- Home Loan Interest Deduction: If the owner has a housing loan on the property, the interest paid on the loan is deductible under Section 24B.

The remaining amount after these deductions is the taxable rental income, which will be taxed as per the applicable income tax slab.

Example of Rental Tax Calculation

Let’s use an example to illustrate the calculation:

- Monthly Rent: Rs 25,000

- Property Tax: Rs 20,000

- Interest on Home Loan: Rs 80,000

Calculation:

| Parameters | Calculation |

| Monthly Rent | Rs 25,000 per month |

| Gross Annual Value (GAV) | 12 (months) x Rs 25,000 = Rs 3,00,000 |

| Property Tax | Rs 20,000 per year |

| Net Annual Value (NAV) | Rs 3,00,000 - Rs 20,000 = Rs 2,80,000 |

| Standard Deduction (30% of NAV) | 30% of Rs 2,80,000 = Rs 84,000 |

| Interest Paid on Home Loan | Rs 80,000 |

| Total Taxable Income | Rs 2,80,000 - Rs 84,000 - Rs 80,000 = Rs 1,16,000 |

This taxable income will then be taxed as per the applicable tax slab.

Properties Not Covered under Rental Income Calculation

Some properties are not included under the rental income taxation. These include:

- Properties inhabited by the owner for personal use (Section 23(2) of the Income Tax Act).

- Farmhouses generating agricultural income (Section 10(1)).

- Properties under local authority possession.

- Properties belonging to political parties (Section 13A).

- Properties owned by members of the Scheduled Castes or Scheduled Tribes.

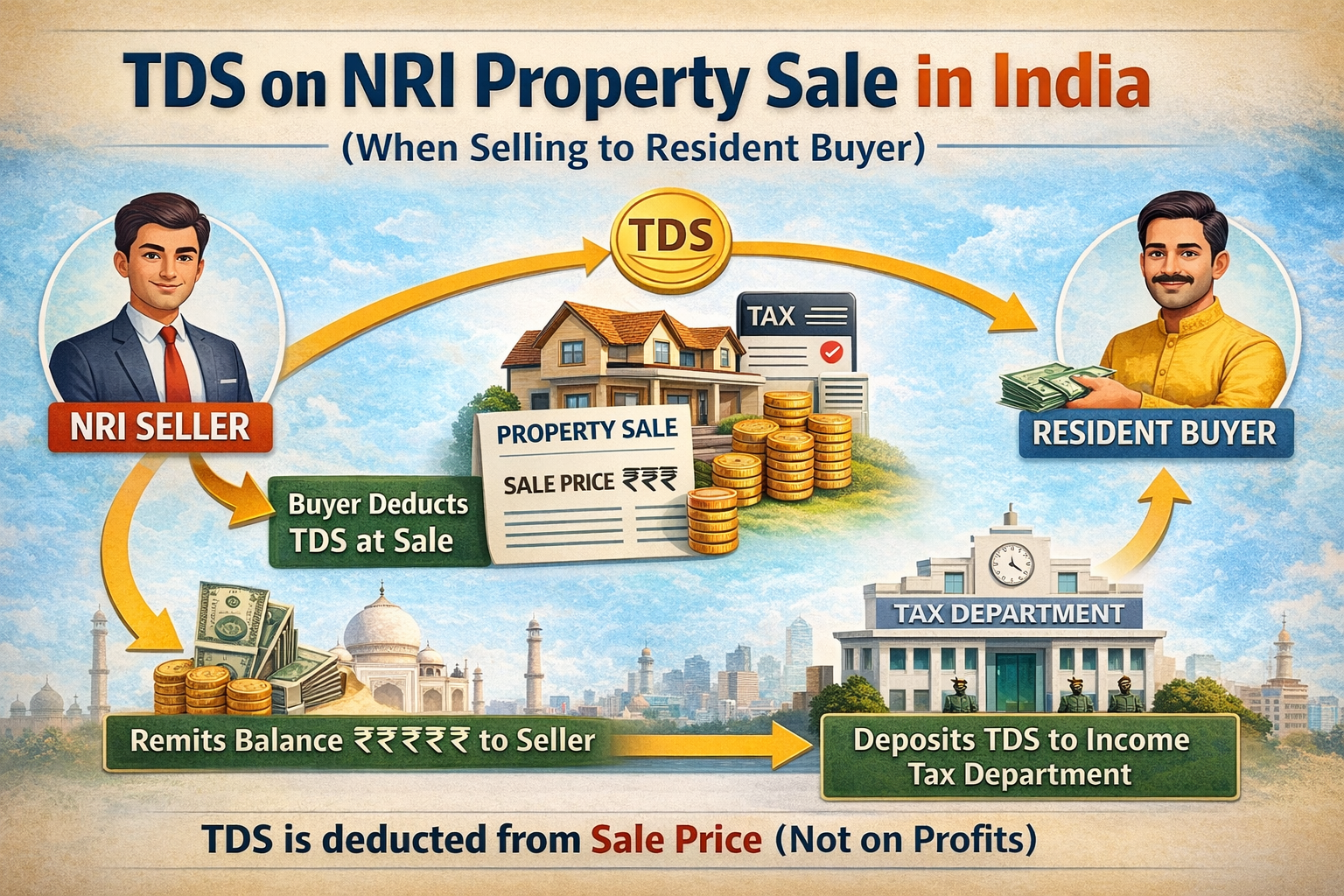

Is Rental Income Earned by NRIs Taxable in India?

Yes, rental income earned by NRIs is taxable under Section 24 of the Income Tax Act. However, the tenant usually deducts the Tax Deducted at Source (TDS) and deposits it with the Indian government. The NRI then submits the TDS form and files Form 15CA to report the transaction.

While NRIs may be subject to double taxation (in India and their resident country), they can claim relief through the Double Taxation Avoidance Agreement (DTAA), if applicable.

How to Save Tax on Rental Income?

There are several ways to save on taxes related to rental income:

- Gross Annual Value Adjustments: Loss of rent due to vacancy or unrealized rent can be adjusted from the total rent receivable.

- Standard Deduction: A 30% standard deduction can be claimed on the NAV of the property.

- Home Loan Interest Deduction: The entire interest on the home loan can be deducted under Section 24B if the property is rented out.

Conclusion

Understanding the nuances of rental income taxation is crucial for property owners to manage their tax liabilities effectively. By leveraging available deductions and exemptions, property owners can significantly reduce their tax burden. It is advisable to consult a qualified tax professional to navigate the specific details of rental income taxation and ensure compliance with the Income Tax Act.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}