Are you a Non-Resident Indian (NRI) planning to sell property in India? Or a resident Indian buyer purchasing property from an NRI?

Understanding the tax implications and TDS (Tax Deducted at Source) compliance is crucial for a smooth and legally compliant transaction.

This article provides a quick-reference guide covering the most important rules and steps involved in such transactions. It is based on common queries from clients and simplifies the process for both sellers and buyers.

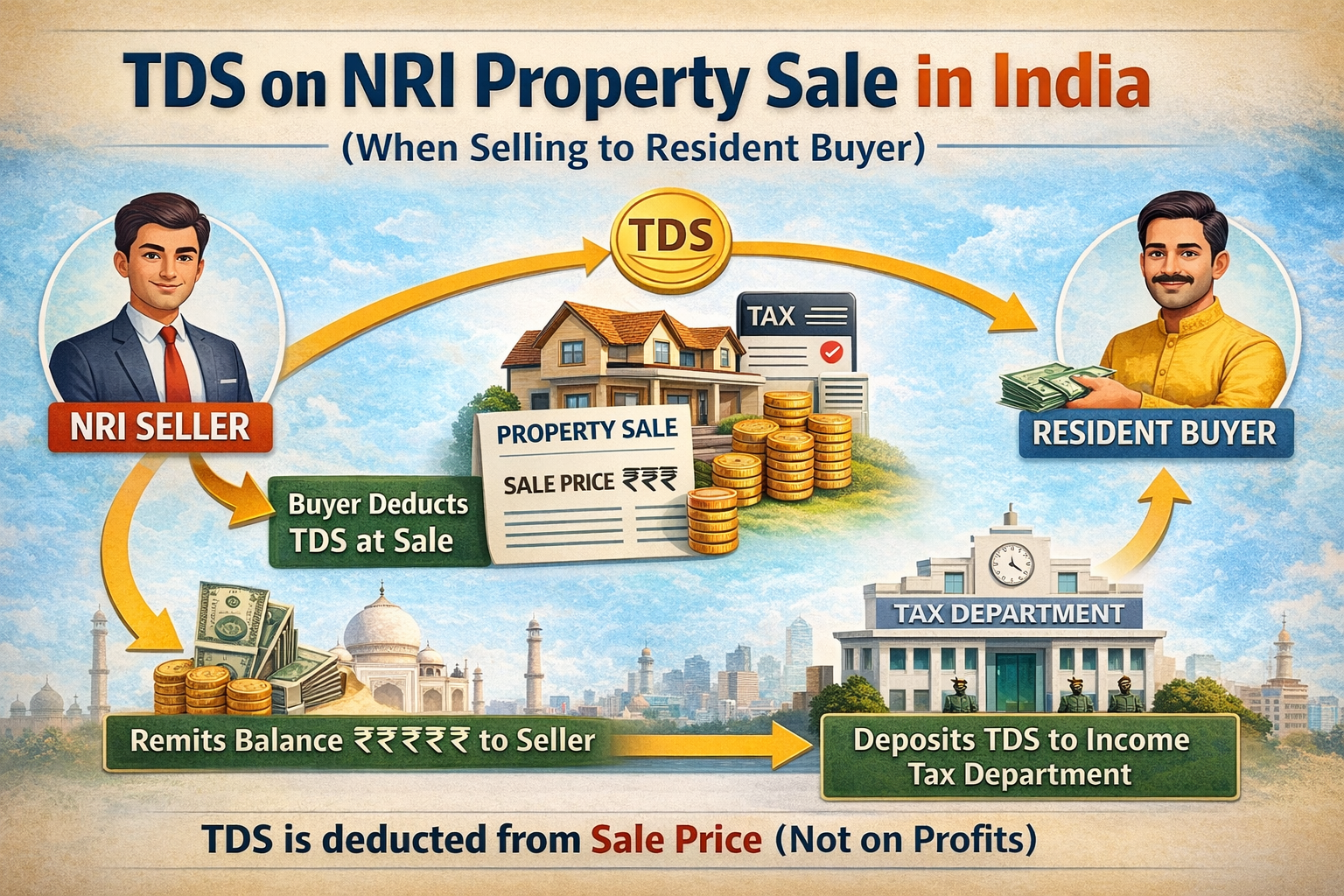

✅ Tax Implications When an NRI Sells Property in India

Whenever an NRI sells property in India, the buyer is required to deduct TDS (withholding tax) on the entire sale value, not on the capital gains.

📌 Example Calculation:

- Sale Value: ₹40,00,000

- Applicable TDS Rate: 13%

- TDS Amount: ₹5,20,000

- Net Payment to Seller: ₹34,80,000

The buyer must:

- Deposit the TDS with the Income Tax Department

- Provide the TDS challan to the seller

- File TDS Return (Form 27Q) at the end of the quarter

- Issue Form 16A (TDS Certificate) to the NRI seller

Later, the NRI seller files their Income Tax Return (ITR) based on actual capital gains and may claim a refund for excess TDS.

📝 TDS Compliance Checklist for Buyers

- TAN Requirement

Buyers must obtain a TAN (Tax Deduction and Collection Account Number) before deducting TDS. It usually takes about one week to receive. - Buyer’s Legal Responsibility

TDS compliance is the buyer's responsibility. Failure to comply can result in penalties and income tax notices. - TDS Payment

TDS must be deposited via the Income Tax e-portal using the buyer’s TAN login. - Seller PAN Not Auto-Linked

The seller’s PAN and name are not automatically shown in the TDS challan. They are only linked after the TDS return is filed. - Penalties for Non-Compliance

Late payment, incorrect filing, or non-deduction can lead to interest and heavy penalties. - TDS Applies to Full Sale Value

TDS is deducted even if there is no capital gain.

📊 Updated TDS Rates (Effective from 23rd July 2024)

| Sale Consideration | TDS Rate |

| ₹0 – ₹50 Lakhs | 13% |

| ₹50 Lakhs – ₹1 Crore | 14.3% |

| ₹1 Crore and Above | 14.95% |

📌 Important Points for NRI Sellers

- Refund of Excess TDS

If TDS deducted exceeds the tax liability, NRIs can claim a refund by filing their ITR. - No Indexation Benefit

As per recent tax rules, indexation benefit is not available to NRIs, potentially increasing taxable gains. - Valuation for Old Properties

If the property was acquired before 1st April 2001, the seller can get it valued as on that date through a certified valuer to reduce capital gains. - Lower TDS Certificate (Form 13)

NRIs can apply for a lower TDS certificate if they want TDS to be deducted on actual capital gains. This process takes time, so advance planning is advised. - Multiple Buyers/Sellers

If there are multiple parties, each buyer must deduct TDS separately for each seller. - Loan-Linked Transactions

In loan cases, banks may require the TDS challan before releasing the funds. Buyers should verify documentation requirements with their lender in advance.

✅ Conclusion: Ensure Smooth Compliance in NRI Property Transactions

Selling property in India as an NRI—or buying from one—requires careful planning, especially regarding TDS compliance, TAN application, and capital gains reporting. With updated tax rates and the removal of indexation benefits, both parties must clearly understand their responsibilities.

- Buyers must deduct and deposit TDS correctly to avoid legal issues.

- Sellers should maintain proper documentation to file tax returns and claim any refunds.

Whether it’s an inherited property, a joint ownership, or a loan-funded deal, early coordination and professional guidance from a tax advisor or CA can help avoid complications and ensure a stress-free property transaction.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}