Non-Resident Indians (NRIs) often face higher tax deductions in India, particularly when selling property or receiving income subject to TDS. Since TDS is deducted on the gross transaction value rather than the actual taxable gains, it can result in excess tax payments. To avoid this, the Income Tax Department provides an option to obtain a Lower or Nil TDS Certificate under Section 197 of the Income Tax Act.

What is a Lower or Nil TDS Certificate?

A Lower or Nil TDS Certificate is an official document issued by the Indian Income Tax Department. It permits the payer—such as a property buyer, tenant, or financial institution—to deduct tax either at a reduced rate or not at all. The certificate is granted after assessing the NRI’s actual tax liability on a specific transaction, ensuring that TDS is aligned with the true tax payable.

What is TDS for NRIs?

Tax Deducted at Source (TDS) for NRIs is governed primarily by Section 195 of the Income Tax Act, 1961. Key provisions of Section 195 include:

- It applies to any person or entity (individuals, HUFs, companies, partnership firms, or other legal entities) making payments to NRIs, irrespective of whether they are taxable in India.

- TDS must be deducted on all payments to NRIs, except for salary (covered under Section 192) and certain interest payments (covered under Sections 194LB, 194LC, and 194LD).

- The deduction must occur at the earlier of:

- Credit of the amount to the NRI’s account.

- Actual payment in cash, cheque, or bank transfer.

- There is no minimum threshold for deducting TDS under Section 195.

Why is it Important for NRIs?

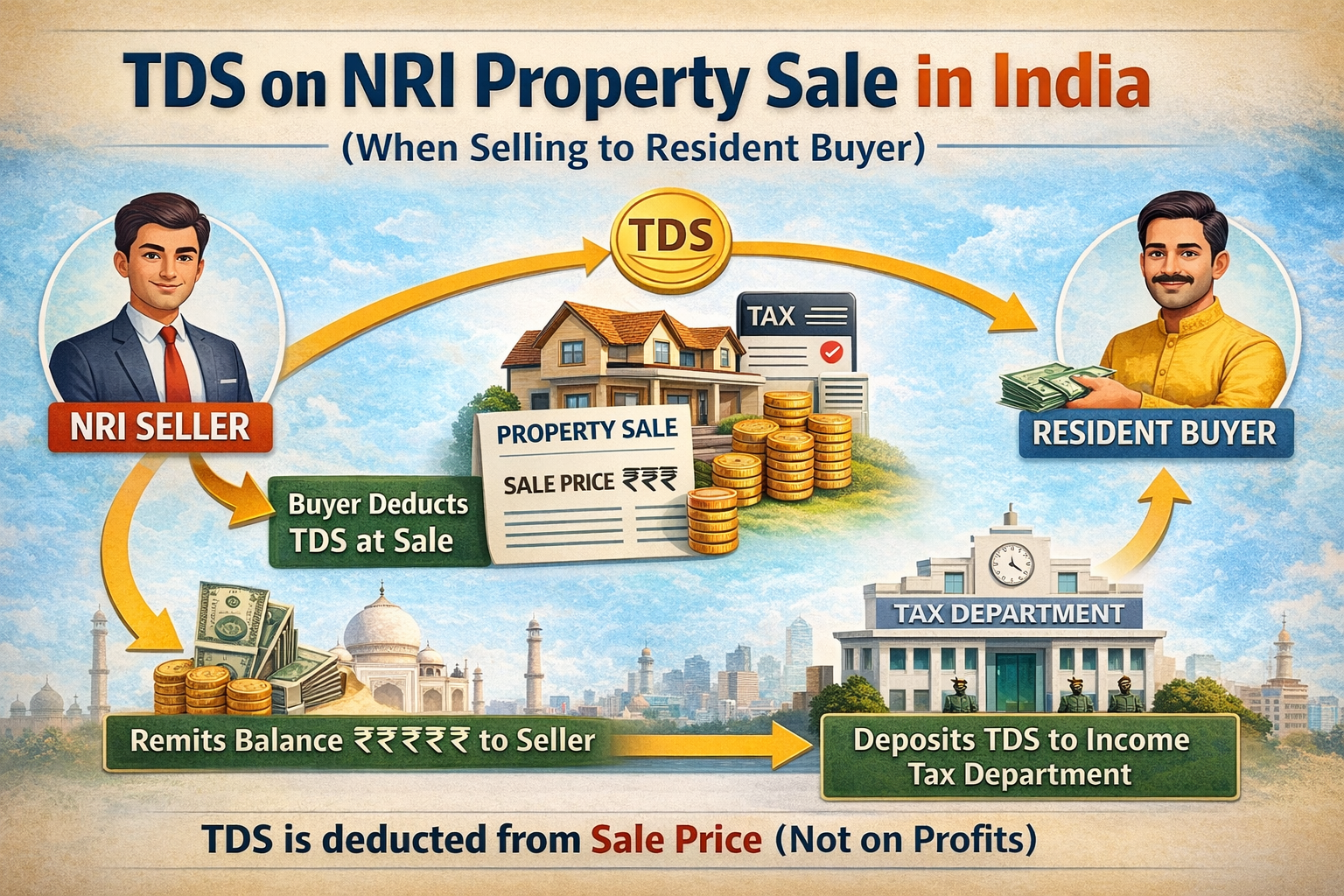

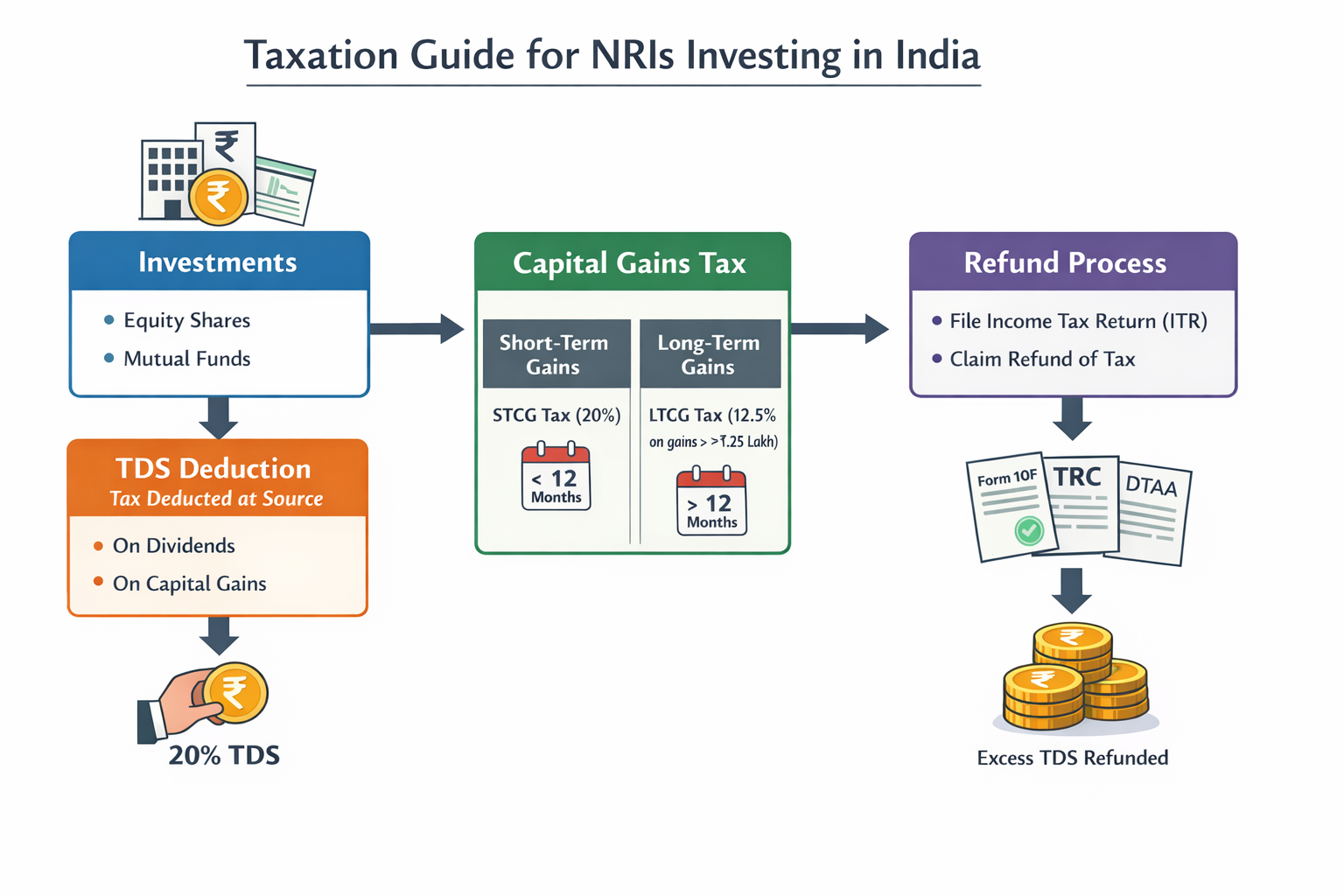

- Avoid Excess Tax Deduction: On property sales, NRIs are subject to TDS at 20% (long-term gains) or 30% (short-term gains) plus surcharge and cess, applied to the entire sale value. This is often higher than the actual tax liability.

- Faster Access to Funds: Without this certificate, NRIs must claim refunds by filing ITR, which delays the release of funds.

- Improved Cash Flow: With a lower or nil TDS rate, NRIs can receive the correct net amount without unnecessary deductions.

When Should NRIs Apply for a Lower or Nil TDS Certificate?

NRIs should consider applying in situations where standard TDS rates exceed the expected tax liability, such as:

- Sale of immovable property in India.

- Rental income from property.

- Interest income from NRO accounts, fixed deposits, or other investments.

- Other income streams where TDS is applicable at a high rate.

Application Process for Lower or Nil TDS Certificate

- Filing Form 13:

NRIs need to submit Form 13 online via the TRACES portal or the Income Tax e-filing portal to request the certificate. - Document Submission:

Supporting documents include:

- PAN card and passport.

- Proof of NRI status.

- Sale agreement or property documents.

- Cost of acquisition and capital gain computation.

- Previous tax returns (if available).

- Bank details and payment proofs.

- Verification by Assessing Officer (AO):

The AO examines the documents, evaluates the actual tax liability, and issues the certificate indicating the applicable reduced or nil TDS rate.

Benefits of a Lower or Nil TDS Certificate

- Correct tax deduction based on actual liability.

- Eliminates refund delays by avoiding excess TDS.

- Enhances liquidity, ensuring smoother financial planning.

- Prevents disputes between buyers, tenants, and NRIs regarding TDS obligations.

Key Points to Remember

- Apply for the certificate before completing the transaction (e.g., property registration or rent payment).

- The certificate is valid only for the specified transaction and time period mentioned.

- In the absence of this certificate, buyers are legally required to deduct TDS at the higher default rates under Section 195.

Conclusion

For NRIs, obtaining a Lower or Nil TDS Certificate is an effective way to prevent excessive tax deductions and streamline financial transactions in India. Professional assistance in preparing accurate capital gains computation and filing Form 13 can significantly speed up the process.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}