Returning to India as a Non-Resident Indian (NRI) involves several financial and tax considerations. Understanding the tax implications, planning strategically, and complying with Indian regulations can ensure a smooth financial transition. This article highlights the essential aspects of tax planning for NRIs returning to India.

Understanding Residential Status

Your residential status under the Indian Income Tax Act determines your tax obligations.

- Resident for Tax Purposes:

You are classified as a resident if: - You stay in India for 182 days or more in a financial year, or

- You stay for 60 days or more in a financial year and 365 days or more in the preceding four years.

Planning your return date is crucial to avoid unintended tax consequences.

- Impact on Taxation:

- Residents: Your global income becomes taxable in India.

- NRIs: Only income earned or received in India is taxable.

Accurately determining your residential status is vital for effective tax planning.

Taxation of Global Income

Once you become a resident, global income—including salary, business profits, and capital gains—becomes taxable in India.

- Foreign Tax Credit:

If you have already paid taxes on foreign income, you may claim a tax credit under the Double Taxation Avoidance Agreement (DTAA) to avoid double taxation. - DTAA Provisions:

These agreements provide relief through tax credits or exemptions, depending on the terms between India and the other country.

Consulting a tax expert ensures compliance and optimal utilization of DTAA provisions.

Declaration of Foreign Assets

Returning NRIs must disclose foreign assets and income in their Indian tax returns.

- What to Declare:

- Bank accounts

- Investments

- Immovable properties

- Other foreign-held assets

Failure to disclose can result in penalties under the Black Money Act. Maintaining documentation and seeking professional guidance ensures compliance.

NRE and NRO Accounts

Tax Treatment of NRE and NRO Accounts:

- NRE Accounts: Balances are repatriable tax-free, but you must convert them to resident accounts upon returning.

- NRO Accounts: Interest earned is taxable, and repatriation is subject to limits and compliance.

Converting these accounts to resident savings accounts within the prescribed timeframe is essential for regulatory compliance.

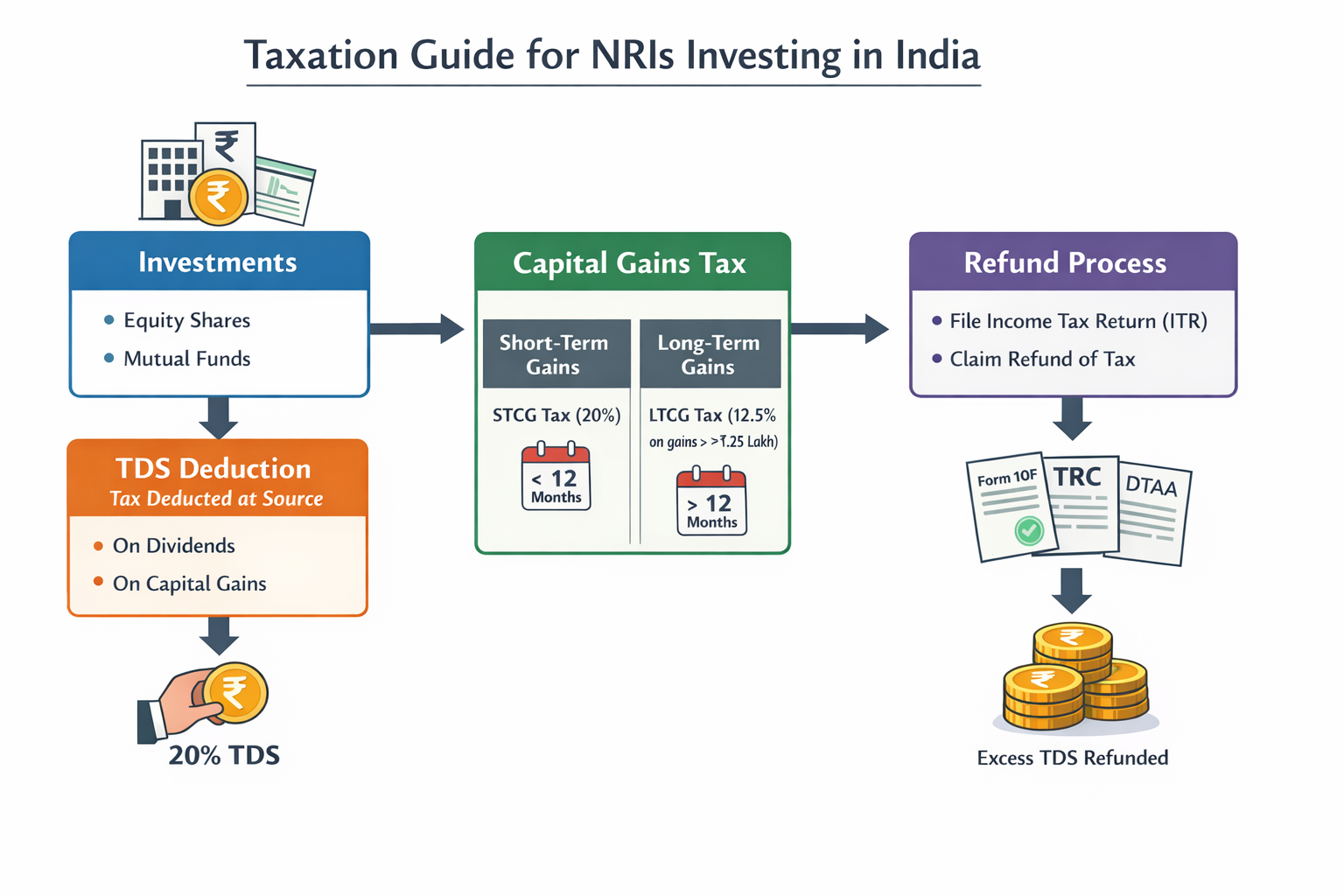

Capital Gains Taxation

Capital Gains on Indian Investments:

- Equity Investments:

Long-Term Capital Gains (LTCG):

- Before: LTCG on listed equity shares held for over 12 months was taxed at 10% above ₹1 lakh.

- After: The tax rate has increased to 12.5%, and the exemption limit has been raised to ₹1.25 lakh. Only gains exceeding ₹1.25 lakh will now be taxed at 12.5%.

Short-Term Capital Gains (STCG):

- Before: STCG on listed equity shares held for less than 12 months was taxed at 15%.

- After: The STCG tax rate has increased to 20%.

- Other Assets (e.g., real estate):

Tax rates vary based on holding periods and asset types.

Capital Gains on Foreign Investments:

If you sell foreign assets after becoming a resident, capital gains are taxable in India. Proper timing and planning of sales can optimize tax liabilities.

Retirement Accounts and Planning

Taxation of Foreign Retirement Accounts:

Funds in accounts like 401(k) or IRAs may be taxable in India, depending on DTAA provisions.

- Options to Consider:

- Maintain the foreign retirement account.

- Transfer funds to an Indian retirement scheme such as the National Pension System (NPS) or PPF.

Seeking professional guidance ensures efficient management of retirement savings.

Tax Deductions and Exemptions

Upon becoming a resident, you gain access to various tax-saving opportunities under the Indian Income Tax Act:

- Popular Tax-saving Investments:

- PPF (Public Provident Fund)

- ELSS (Equity Linked Savings Scheme)

- Life Insurance Premiums

- Deductions under Key Sections:

- Section 80C: Investments in specified instruments.

- Section 80D: Health insurance premiums.

- Section 24(b): Home loan interest payments.

Strategically planning investments helps maximize deductions and minimize tax liability.

Advance Tax Payments

If your total tax liability exceeds ₹10,000 in a financial year, paying advance tax is mandatory.

- Instalments: Advance tax must be paid in specified instalments.

- Consequences of Non-payment: Failure to pay advance tax or underpayment attracts interest penalties.

Estimating your tax liability accurately helps avoid penalties and ensures compliance.

Professional Assistance for Tax Planning

Given the complexities of tax laws for NRIs, seeking professional advice is highly recommended.

- Why Engage a Tax Expert?

- Tailored strategies to optimize tax liability.

- Guidance on compliance with asset declarations and regulatory requirements.

- Assistance with leveraging DTAA benefits and advance tax planning.

Choosing a consultant with expertise in NRI taxation ensures a seamless transition and sound financial management.

Conclusion

Returning to India as an NRI involves navigating intricate tax regulations, planning finances, and ensuring compliance. Understanding your residential status, global income taxation, and investment implications can help you optimize your tax liability and avoid penalties. With proper planning and the support of a qualified tax professional, you can ensure a smooth financial transition and make the most of your return to India.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}