{kind=link}

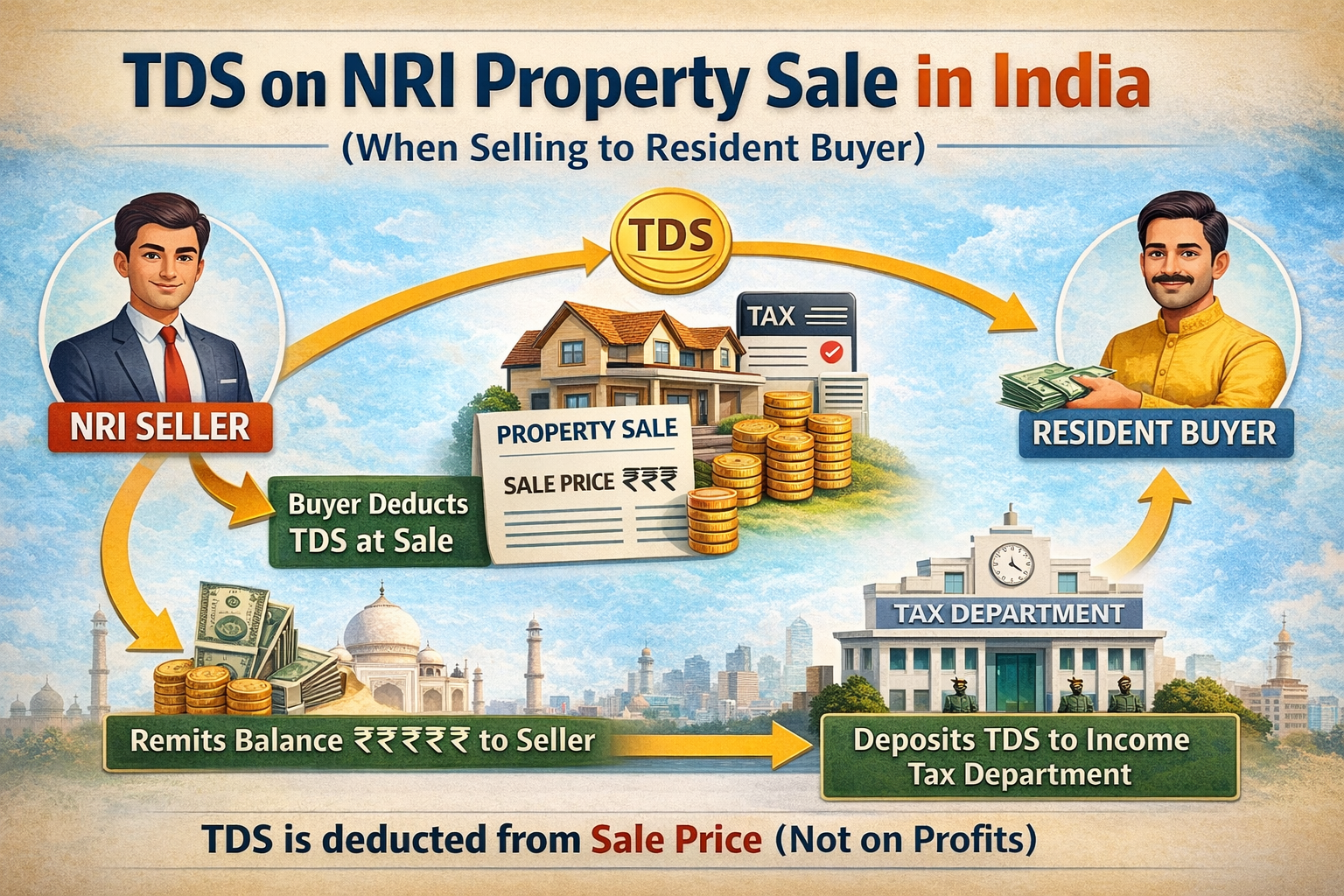

The Union Budget 2026 has introduced important tax reforms and compliance relief measures for Non-Resident Indians (NRIs). If you are an NRI living in the USA and planning to sell property in India, these Budget 2026 NRI updates directly impact your transaction. While capital gains tax rates remain unchanged, the government is trying to […]

{kind=link}

If you are an NRI living in the United States and planning to sell property in India, understanding capital gain tax in India for NRIs in USA is extremely important. Many NRIs assume taxation works the same way as for resident Indians — but that is not true. This guide explains everything you need to […]

{kind=link}

Introduction: Living and working in the USA offers higher salaries, new opportunities, and a global lifestyle. But many NRIs assume that being abroad automatically exempts them from Indian taxes. The truth? Misunderstanding your residential status can lead to costly mistakes, from unexpected tax bills to penalties. Before diving into common pitfalls, it’s important to […]

{kind=link}

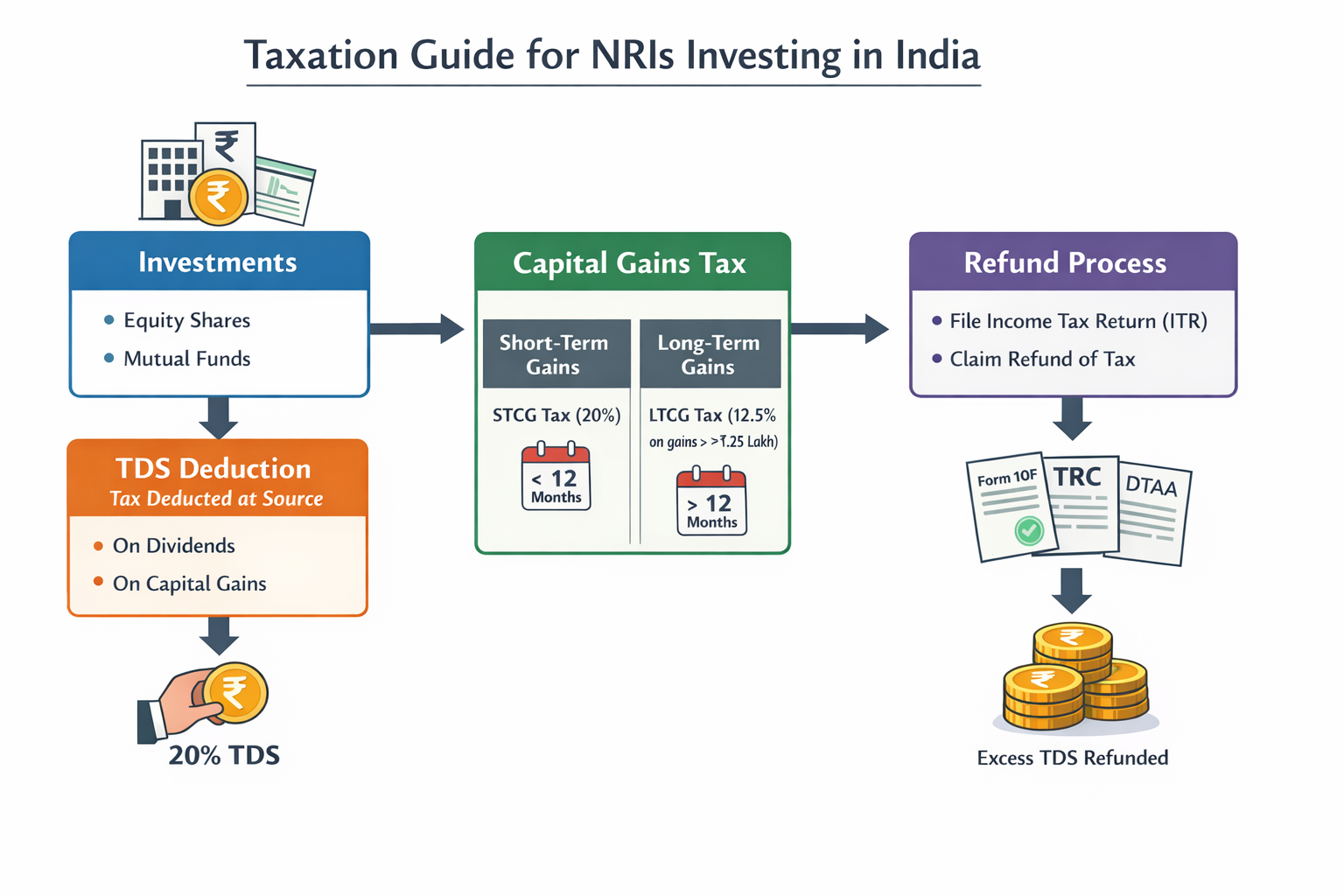

Indian mutual funds and equity markets present lucrative investment opportunities for Non-Resident Indians (NRIs). However, income taxation rules for NRIs differ significantly from residents, and understanding these provisions is essential to optimize returns. Mandatory TDS, capital gains tax, and other tax income implications directly affect profitability. This guide covers the taxation of shares and […]