Section 195 of the Income Tax Act mandates the deduction of Tax Deducted at Source (TDS) on payments made to non-residents (excluding companies) or foreign companies if such payments are taxable under Indian law. Details of these transactions must be reported in Form 15CA. Before remitting funds, the payer must file this form, which can be submitted both online and offline. In specific cases, a Chartered Accountant’s certificate in Form 15CB is also required.

This article delves into the scope, significance, and compliance requirements under Section 195 of the Income Tax Act.

What is Section 195 of the Income Tax Act?

Section 195 of the Income Tax Act, 1961, deals with the deduction of TDS on payments made to non-resident Indians (NRIs). It ensures the prevention of double taxation and determines applicable tax rates for business transactions involving NRIs. TDS is deducted either at the time of crediting the payment to the non-resident’s account or when the payment is made.

Scope and Importance of Section 195

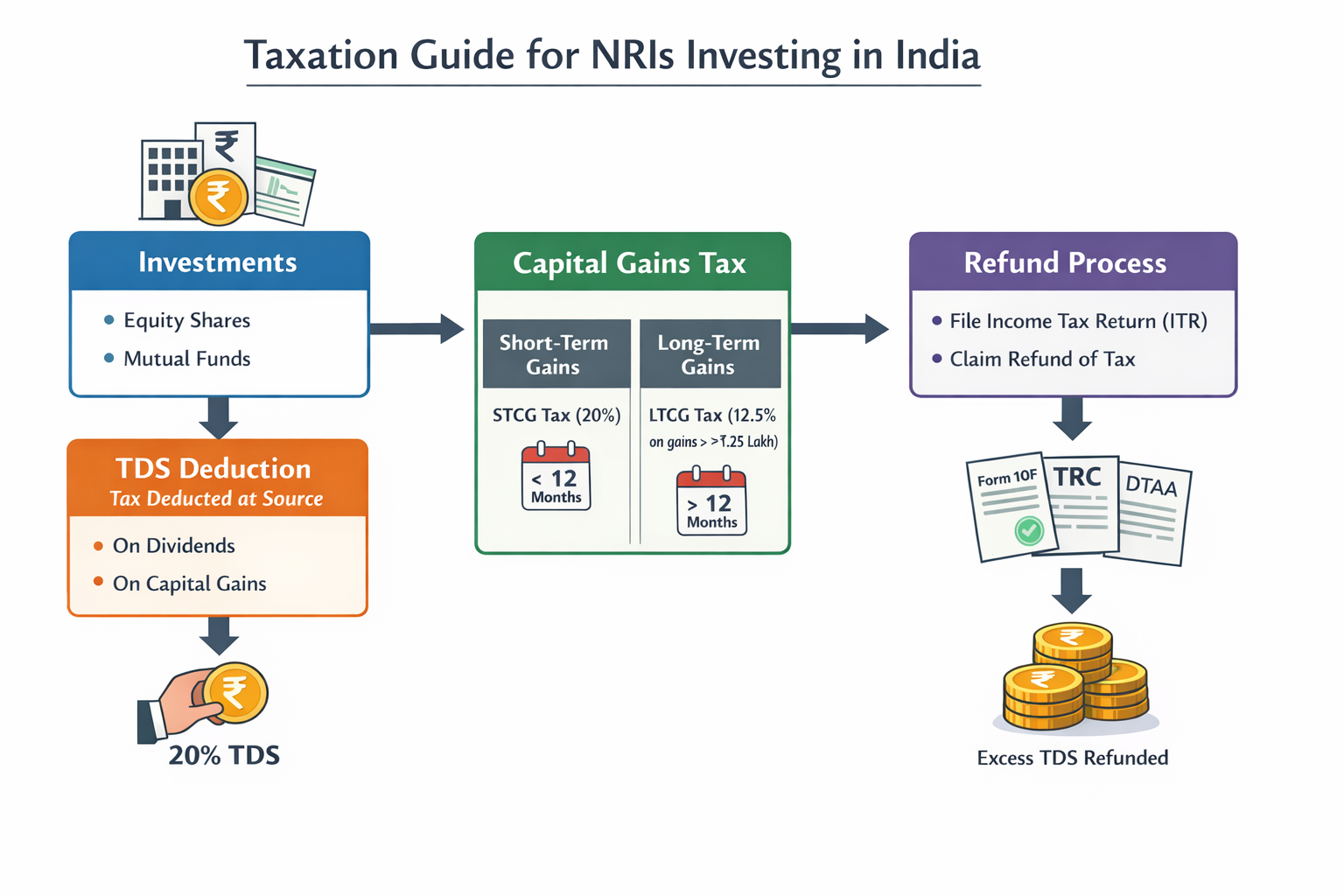

- It applies to various payments made to non-residents, including interest, dividends, royalties, and fees for technical services.

- It governs cross-border transactions involving NRIs and foreign companies.

- TDS rates under Section 195 depend on the nature of income and any provisions under Double Taxation Avoidance Agreements (DTAAs).

Compliance and Reporting under Section 195

- All individuals and entities making taxable payments to non-residents must comply with this section.

- TDS must be deducted at prescribed rates before making any payment to the non-resident.

- Under Section 195(2), payers can approach the Assessing Officer for clarification on the portion of income subject to TDS and the applicable rate.

Distinct Features of Section 195

- Specifically focuses on payments to non-residents and addresses complexities in international financial transactions.

- Ensures tax collection on income earned in India by non-residents.

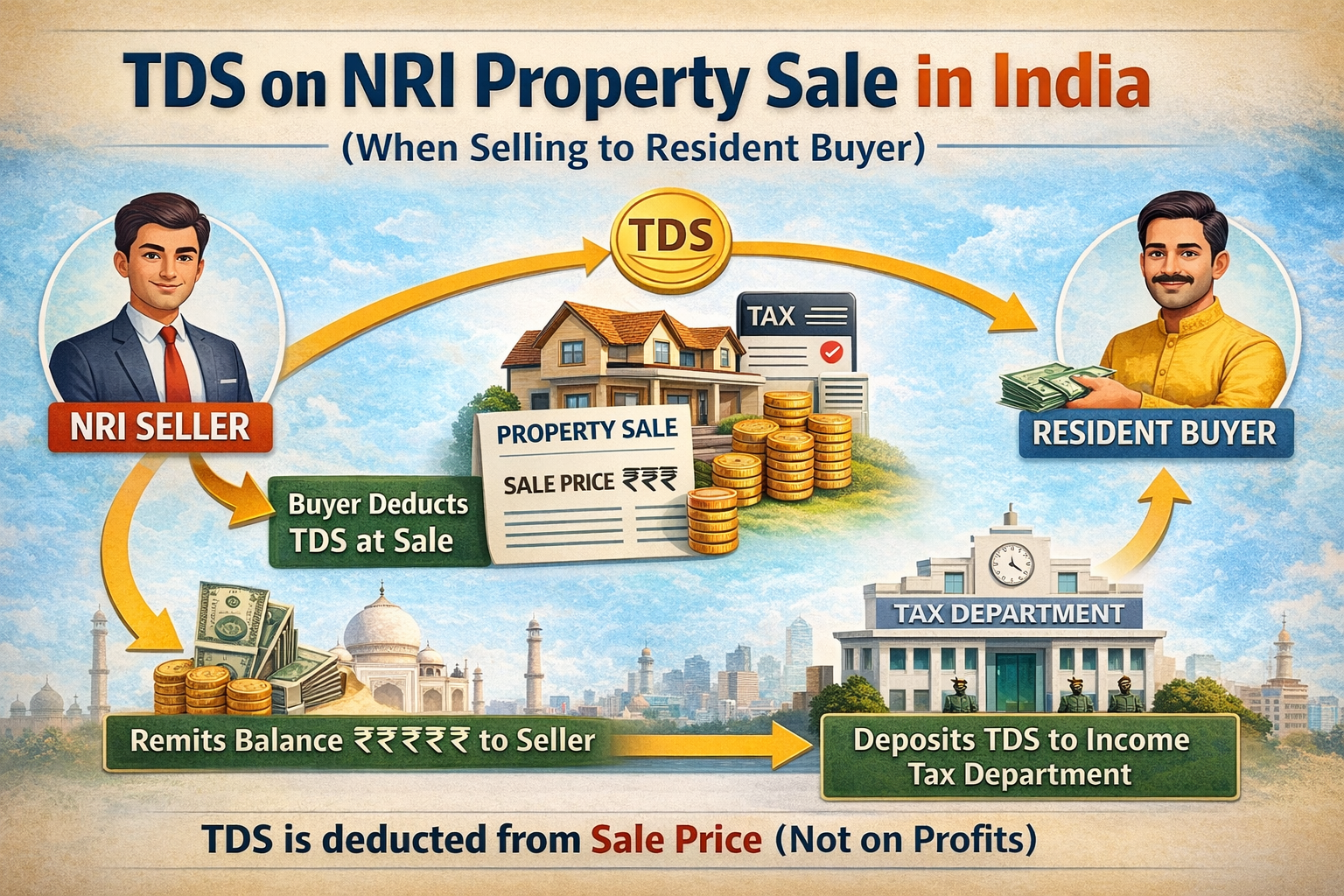

- Includes provisions for real estate transactions, requiring TDS deduction on property sales proceeds paid to non-residents.

Example of Section 195 in Practice

Suppose an Indian resident has business transactions with an NRI. If the payment is taxable in India, the payer must deduct TDS on the payment to allow the NRI to fulfill their tax obligations. Once deducted, the TDS must be deposited with the Indian government within the specified timeline.

NRIs can apply for certificates from tax authorities for a lower or nil TDS rate.

Who is a Non-Resident?

Under the Income Tax Act, a person qualifies as a non-resident if they do not meet the residency criteria outlined in Section 6:

- They are in India for less than 182 days during the financial year, or

- They are in India for less than 60 days during the financial year and less than 365 days in the preceding four years.

Exceptions for Indian Citizens or Persons of Indian Origin (PIOs):

For individuals whose income (excluding foreign sources) exceeds ₹15 lakhs:

- The 60-day threshold is extended to 120 days.

- If leaving India for employment, the threshold increases to 182 days.

Entities Responsible for Deducting TDS

The following entities must deduct TDS under Section 195:

- Individuals

- HUFs

- Partnership firms

- NRIs with income chargeable in India

- Foreign companies

- Juristic entities

How TDS is Deducted under Section 195

- Obtain TAN: Payers must obtain a Tax Deduction Account Number (TAN) by submitting the required forms with the PAN details of both the payer and NRI.

- TDS Deduction: TDS is deducted from the payment and mentioned in the sale deed for property transactions.

- Deposit TDS: Deducted TDS must be deposited with the government via authorized banks or online, before the 7th of the following month.

- Issue TDS Certificate: The payer must issue a TDS certificate (Form 16A) to the NRI within 15 days of filing the TDS return.

TDS Rates Under Section 195

| Type of Income | TDS Rate |

| Payments from investments | 20% |

| Interest on foreign currency loans | 20% |

| Long-term capital gains | 10% |

| Capital gains under Section 115E | 10% |

| Other long-term capital gains | 20% |

| Short-term capital gains under Section 111A | 15% |

| Technical services payments | 10% |

| Royalties paid by Indian citizens | 10% |

| Royalties from other sources | 10% |

| Other sources of income | 30% |

Key Steps for Compliance

- TAN Acquisition: Obtain a TAN before deducting TDS.

- Timely Deduction: Deduct TDS when crediting the payment or at the time of actual payment.

- Deposit Timeline: Deposit TDS before the 7th of the next month.

- Quarterly Filing: File TDS returns (Form 27Q) quarterly.

- Certificate Issuance: Issue Form 16A within 15 days of the TDS return filing deadline.

Implications of Non-Compliance

Failure to deduct and deposit TDS under Section 195 may result in:

- Disallowance of expenses in the year of payment.

- Interest at 1.5% per month on late deposits.

- Penalty under Section 221 or Section 271C for non-deduction or partial deduction.

Conclusion

Section 195 of the Income Tax Act ensures proper taxation on payments to non-residents, safeguarding compliance with Indian tax laws. It is essential for businesses and individuals making such payments to adhere to the provisions to avoid penalties and legal repercussions. To navigate the complexities of Section 195 and ensure compliance with its provisions, seeking professional assistance is highly recommended.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}